Using AI to Identify Underserved Communities for Microfinance Investment

By Alisha Srivastava, Northeastern University

Introduction

Over 1.4 billion people globally remain unbanked, according to the World Bank, limiting their ability to access loans, build credit, or save securely. Financial exclusion is a significant barrier to economic mobility, especially in low-income and rural communities. Even though traditional microfinance initiatives have tried to address this issue, many have been unsuccessful because of poor targeting, misallocated funds, and unsustainable lending models. As a result, many people do not have access to reliable financial services, limiting their ability to invest in their futures.

Artificial intelligence (AI) offers a new way forward. By leveraging data-driven insights, AI can more effectively identify underserved communities and design tailored financial solutions. Through AI, companies can improve access to financial services, enhance risk assessments, and increase overall operational efficiency, in turn making financial inclusion more achievable.

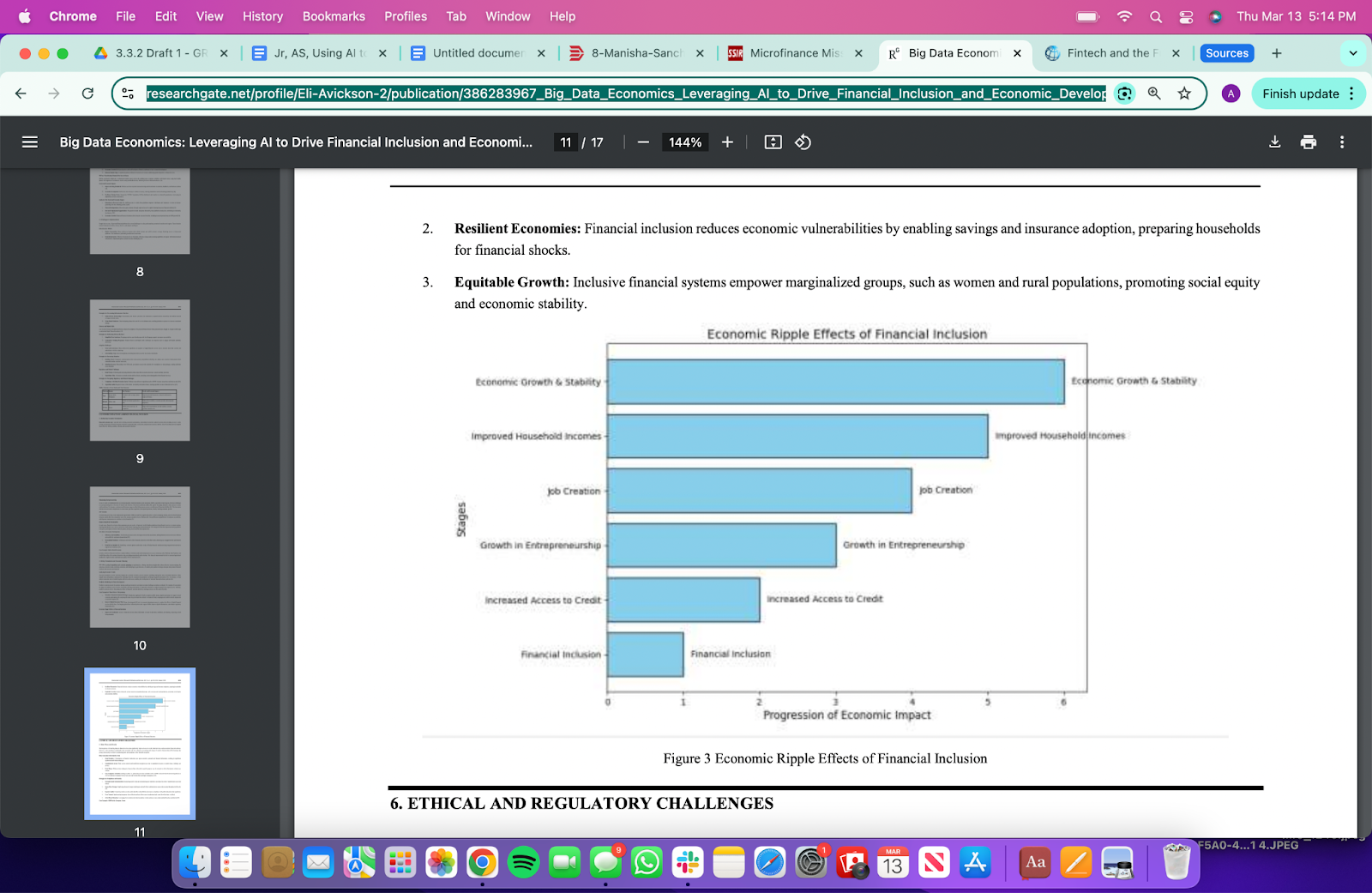

Economic Ripple Effects of Financial Inclusion from the source Big Data Economics

How AI Can Support Microfinance for Underserved Communities

AI can significantly improve financial inclusion by making microfinance more efficient, scalable, and personalized. One way it achieves this is by automating processes like loan approvals, risk assessments, and fraud detection. This automation reduces costs, which then allows microfinance companies to reach a broader audience without compromising on the quality of service. In addition, AI allows for creating personalized financial solutions by analyzing data sources like mobile transaction history or spending habits. This helps organizations design financial products that are tailored to people who might not meet the traditional lending criteria.

In a self-conducted interview conducted with Scott Bradley, Vice President of AI at Novartis, he emphasized that AI has been particularly useful in identifying underserved populations by analyzing large datasets. In the healthcare sector, AI helps recognize patients who are not receiving full medical treatment. This same strategy can be applied to microfinance by AI detecting people who lack access to traditional banking but show patterns of financial responsibility through alternative data sources.

AI's skill in identifying economic patterns and market trends also improves data-driven decision-making. It can understand which businesses or industries within a community are struggling and recommend targeted financial support, which then helps in driving economic growth and stabilizing economies. This not only benefits people receiving financial aid but also strengthens local businesses and communities, creating a cycle of economic growth. By delivering the right solutions at the right moment, AI can make sure that resources are going where they are needed the most. It fosters long-term sustainability and strengthens financial resilience, especially in underserved communities.

The World Bank emphasizes how AI can reshape the future of finance through improving access and reducing inefficiencies. With the use of digital financial identities, AI helps people without traditional banking histories have secure access to loans and financial services. It also improves transparency by detecting fraud and making sure funds are used properly, which helps microfinance institutions direct resources to those who are in need. By increasing trust and accountability, AI can help in bridging the gap between financial institutions and the communities they are serving, making sure that microfinance is both ethical and impactful. This can ultimately make financial systems more inclusive and beneficial for underserved populations.

However, Scott Bradley also pointed out that while AI has the potential to improve financial inclusion, it must be implemented carefully to avoid unintended exclusion. He explained that AI is highly data-driven, which means it could overlook certain populations if the data used to train models is not representative. In microfinance, AI can improve matchmaking between lenders and borrowers by leveraging alternative data sources, such as bill payment histories and spending patterns, but only if these models are designed with inclusivity in mind.

Challenges Facing AI in Microfinance

A lot of microfinance projects have failed to make a real impact because microfinance does not always reduce poverty. Many microloans are used to support small businesses, but these businesses do not always make enough income to lift people out of poverty. In addition, high interest rates can make repayment hard, which can trap borrowers in a cycle of debt instead of helping them grow financially. Many times, microloans are used for personal expenses instead of being invested in businesses, with people then using the money for daily needs like food, medical bills, or school fees. Another issue is that some microfinance institutions prioritize profits over truly helping low-income communities, which then diminishes the overall impact of microfinance. Instead of relying only on loans, combining financial services with education, savings programs, and better social policies can have a more significant and lasting effect on reducing poverty.

Scalability in microfinance can be a big challenge, especially because of manual processes like loan approval and risk assessment. These processes are usually slow and have high costs, which makes it difficult for microfinance initiatives to expand their reach. As a result of this, many organizations struggle to provide financial services to more people in need, limiting their impact, especially in underserved communities. This inefficiency prevents microfinance from being a sustainable long-term solution, which is why AI-driven automation is so promising in transforming the industry.

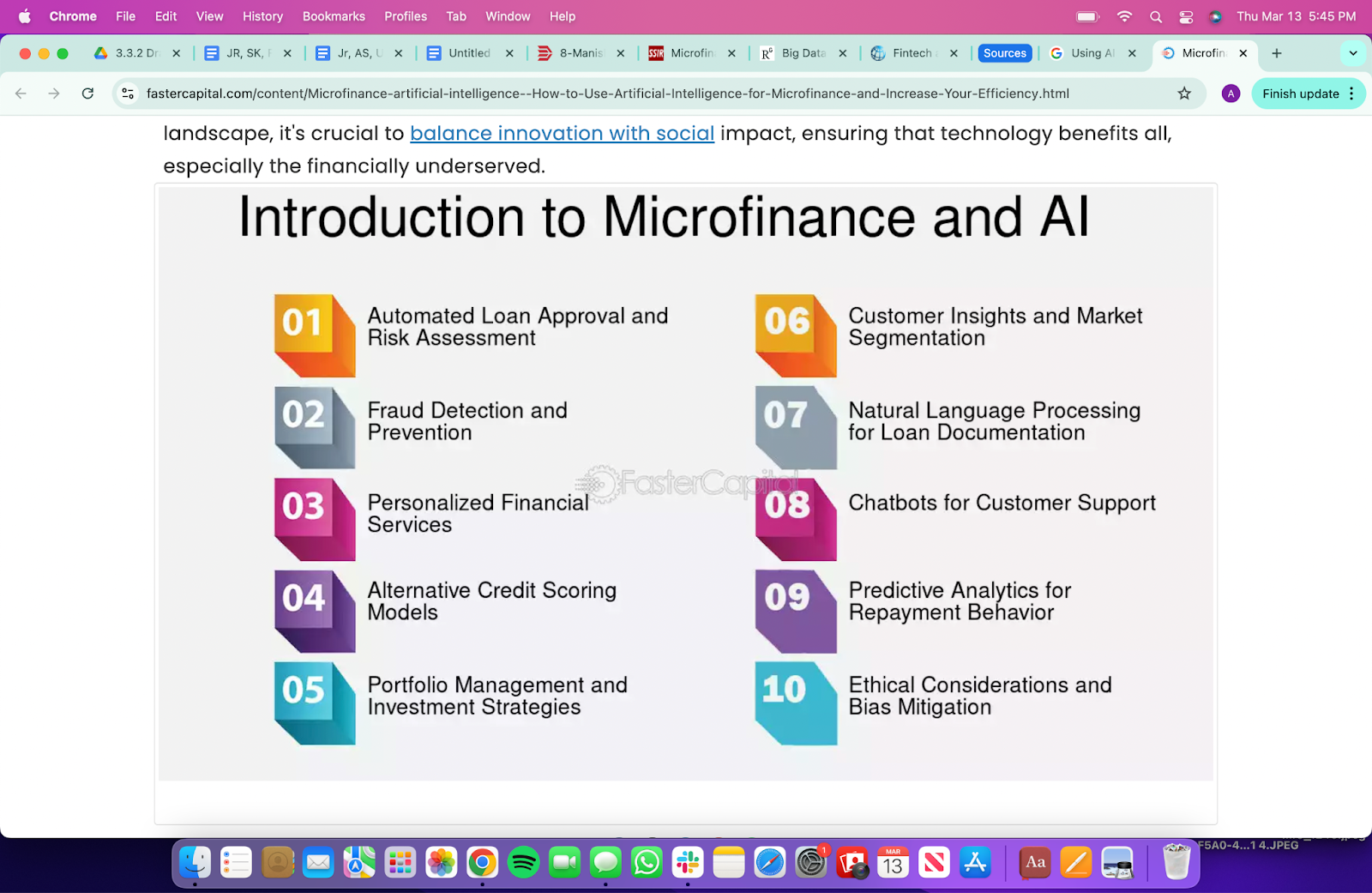

How to use artificial intelligence for microfinance and increase efficiency from the source Faster Capital

AI Bias & Transparency

AI-driven models for financial inclusion have not always been successful, due to several key challenges. A major issue is the bias in the data used to train AI systems, which can lead to skewed decision-making that disproportionately brings harm to marginalized communities. These biases often come from historical data that reflects existing inequalities.

Another challenge is the lack of transparency in AI decision-making processes. Without clear explanations for AI-driven financial decisions, people can struggle to trust the systems that are meant to assist them. This limits AI’s effectiveness in financial inclusion initiatives. To fully understand AI's potential for underserved communities, there needs to be improved data quality, biases need to be addressed, and transparency is needed in how decisions are made. By doing these three things, AI can more effectively cater to those who need the financial support the most.

Scott Bradley highlighted that bias is a persistent challenge in AI, even in fields like healthcare, where clinical trial data can sometimes under-represent certain populations. He explained that one way to mitigate bias is by making sure that AI models are validated against diverse datasets, which helps improve accuracy and fairness. In addition, he noted that AI can actually be used to detect and reduce bias in other AI-driven systems, and that financial institutions could leverage AI to fix their own models for potential discriminatory patterns.

Transparency is a critical factor in building trust in AI-driven financial inclusion initiatives. According to Scott Bradley, most AI-related biases are not consumer-facing but instead impact internal business decisions, such as marketing campaigns or operational strategies. He suggested that organizations should focus on addressing these biases early in the AI development process, which can help lead to more transparent and equitable financial inclusion efforts.

Conclusion

AI has the ability to address the issues within microfinance and create more efficient, scalable, and personalized financial solutions. In the past, traditional microfinance models have failed because of poor targeting, high interest rates, and the misallocation of funds. However, AI can overcome these challenges by automating processes like loan approvals and fraud detection, which reduces costs and allows microfinance institutions to reach underserved communities. By utilizing alternative data and identifying economic patterns, AI can create financial products that are better suited to the needs of these populations.

In addition, AI's role in improving transparency and detecting bias is essential to ensuring fairness in financial services. AI-driven digital financial identities can help people without traditional banking histories gain access to essential services. Even though AI models have faced challenges in the past, such as biases in data and lack of transparency, addressing them through better data practices and algorithm transparency will make AI a powerful tool in driving financial inclusion, providing opportunities for economic growth and financial security to underserved communities.

| A guest post by

|